Get 3D Rendering For Dwelling

Make Informed Design Decisions Showcase Your Design Ideas

Get Rendering

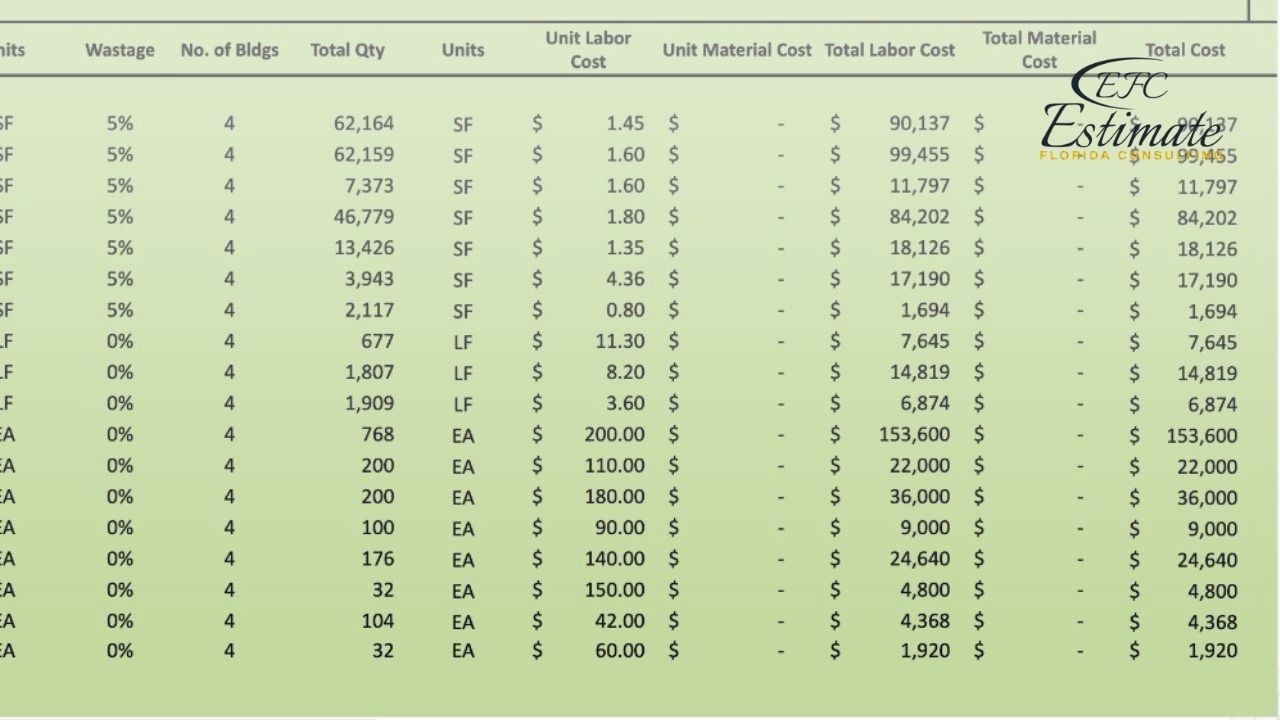

Winning Bids Made Easy – Get Your Dwelling Complex Estimates Today!

Fast, accurate, and tailored to your project's zip code. Secure more wins – try it now!

Upload Plan

I used their services for estimation. I am really impressed with their services. Thank you for your good service.

I used their services for estimation. I am really impressed with their services. Thank you for your good service.

I used their services for estimation. I am really impressed with their services. Thank you for your good service.